Tariffs, Tech Cycles, and a New Economic Reality

Global markets are entering a new chapter, one that demands a shift in how early-stage investors operate. This issue breaks down the structural forces reshaping the macro and technology landscape – and how value is set to accrue differently going forward.

01 | A new economic paradigm

I’ve spent the past few weeks trying to make sense of the shifting economic landscape, and what it means for technology markets. Bridgewater’s recent newsletter, “Adapting to a New Reality,” offers a bold take on this moment:

To state the obvious: we are now facing a radically different economic and market environment that threatens the existing world order and monetary system... This new macroeconomic and geopolitical paradigm is turning past tailwinds into headwinds and reshaping global flows of capital.

If you were to list the defining characteristics of recent decades and compare them to today, you’d struggle to find much overlap. We have been through many big economic shifts over Bridgewater’s 50-year history, so we don’t speak lightly when we say that this looks like a once-in-a-generation one.

There is still a lot of uncertainty around the degree and pace of change. But the trajectory is becoming increasingly clear – we’re entering a new environment, unlike anything most of us have invested or operated in before.

For technology and venture investors, I don’t think this requires a full reset. But it is a moment for first-principles thinking:

→ How is the macro environment changing?

→ Where are we in the technology cycle?

→ And therefore, how does the venture playbook need to adjust?

02 | How is the macro environment changing?

Two fundamental shifts are currently underway in the political economy:

Fragmentation of global alliances and supply chains, which could drive down U.S. equity prices.

Growing risk of U.S. stagflation.

Both will fundamentally redirect capital flows and reshape overall demand.

A | Globalization → balkanization

For the past decade, U.S. stocks have soared, lifted by decades of global trade and easy, cross-border investment. Today, U.S. equities trade at a 70% premium to the rest of the world — meaning they need to attract about 70 cents of every new dollar invested in global equities just to maintain their current value.[1]

This is an extreme requirement, a higher bar than we’ve seen at any point in the last half-century.

Source: Eaton Vance

For U.S. equities to sustain these valuations, two factors must hold:

A large and persistent capital surplus, meaning foreign investment into U.S. assets must continue to significantly exceed U.S. investment abroad.

Continued access to global markets. Today, foreign demand is driving a meaningful (and growing) share of U.S. company’s revenue and earnings.[2]

Trump’s agenda — reversing trade deficits, U.S. self-sufficiency, and tighter government control over industries like energy and defense — poses a significant threat to both. The recent U.S. Treasury sell-off and rising yields are early signs of this strain taking hold.

To be clear, Trump’s policies are simply the latest (and unnecessarily chaotic) expression of this trend. But international decoupling has been building for years. Global trade restrictions have tripled since 2018. And even Biden-era policies like the CHIPS and Inflation Reduction Acts reinforce a broader trend toward reshoring and national self-reliance.

As globalization fractures, expect a compression in U.S. asset prices. The biggest impact and pain will be felt in the most concentrated parts of the market: (a) public tech megacaps, and (b) exits for late-stage private tech companies, especially those with stretched valuations, additional scale requirements to hit profitability, and cash reserves that can be traced back to foreign investment.

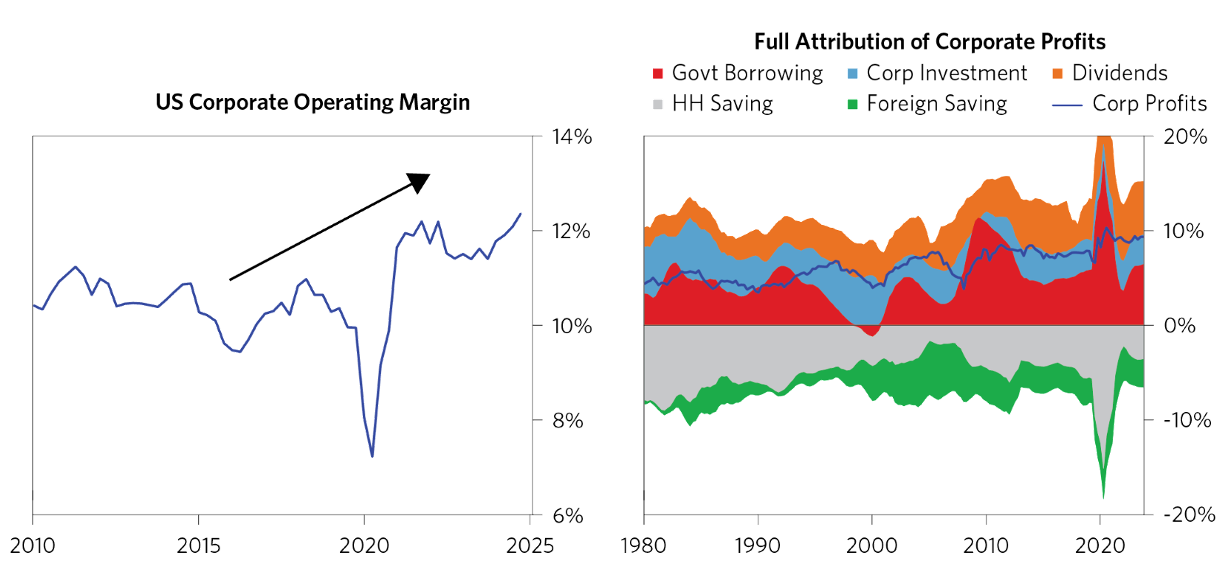

B | The risk of stagflation

Over the past decade, U.S. equities were buoyed by strong growth and earnings, fueled in part by government borrowing. Modest growth in tax receipts, rising expenditures, and strong foreign demand for Treasuries allowed the U.S. to run large deficits without major consequences.[3]

This borrowing injected liquidity into the economy, boosting household demand and, in turn, driving steady growth in corporate revenues and profit margins.

Source: Bridgewater. “The Growing Risk of U.S. Assets.” Mar 6, 2025.

Today, that dynamic – which American workers, consumers, and investors have long taken for granted – is under threat.

Rather than expanding the tax base, the current administration is pursuing aggressive spending cuts through DOGE, the upcoming tax bill, and a commitment to public sector deleveraging.

If government borrowing falls, household demand and business performance will likely weaken. And unless private sector borrowing rises sharply to make up for the gap — unlikely given tighter credit and waning consumer confidence — economic growth will slow. At the same time, new tariffs (both U.S.-imposed and retaliatory) are adding inflationary pressure.

If these trends hold, there’s a real risk of stagflation, which would leave the Fed constrained, unable to stimulate the economy without worsening price pressures.

This isn’t a comfortable diagnosis. But I do believe a more clinical understanding of these dynamics, combined with a clear sense of where we are in the tech cycle, can help investors navigate the road ahead — and capture value while others hit pause or cling to the old playbook.

03 | Where are we in the technology cycle?

Technology innovation evolves in 10–15 year cycles, usually somewhat independent from broader macro forces:

Phase 1 Each cycle begins with a breakthrough that creates a step-change in capability, followed by a short-term surge of excitement, over-investment, and an eventual crash.

Phase 2 New, open standards emerge, enabling broader distribution and sustainable adoption. Commercial applications are built on top of those standards, organizing users, data, and transactions in new ways to capture value, and entrenching themselves through network effects and scale.

Phase 3 As adoption matures, the underlying technology hits market saturation. The marginal gains of using the technology shrink, and asymmetric upside fades. A new breakthrough is needed to restart the cycle.

Each cycle builds on the infrastructure of the last, so the opportunity for value creation grows larger with each subsequent wave.

Today, we are entering a new era of intelligent compute, somewhere between Phase 1 and Phase 2.

The transformer model triggered a step-change in machine intelligence, catalyzing early excitement and a surge of investment. But most AI startups today still rely on proprietary models they don’t control, and cloud infrastructure built for static data and human-centric workflows.

Going forward, durable innovation will require new, open standards that can scale AI natively across industries, not just patch it onto legacy systems.

Today’s moment in technology evolution parallels the late 1990s, before the dot-com bubble. But the financial and competitive conditions are meaningfully different, suggesting history won’t repeat itself in exactly the same way:

The opportunity is larger. If historical patterns hold, the total addressable surface for new AI applications should be multiples larger than last cycle, as AI unlocks broader capabilities and pushes software deeper into workflows that were previously out of reach.

The incumbents are stronger. They are software-native, not legacy industrial models. Big Tech still owns distribution, compute, and capital. These incumbents can iterate faster and absorb innovation more efficiently than what we’ve seen in prior cycles.

Private markets are more robust. Illiquidity, dry powder, and momentum-based psychology have delayed the normal flushing out of risk, making a sharp “crash” less likely.

04 | How does the venture playbook need to adjust?

To summarize, U.S. technology markets are facing the following dynamics:

As the U.S. pulls back from the global economy, asset prices, especially in late- and megacap tech, are likely to fall. Expect a lower ceiling on valuations going forward.

The U.S. economy is slowing, with businesses and consumers facing higher costs, weakening demand, and early signs of waning access to global markets and capital.

We are in the early phases of a new technology cycle. As AI permeates the economy, it will unlock entirely new markets and power economic growth. But in the near-term, private market dynamics may continue to mask fragile business models. Early-stage investors who see this clearly will avoid the worst excesses.

Startups today are competing against software-native incumbents. Without structural product innovation – new architectures, new data sets, new methods for interoperability – it will be difficult for startups to maintain a durable edge.

All that said, early-stage venture remains an attractive category.

It has always been more insulated and idiosyncratic than other alternative assets. It usually represents only a small slice of portfolios and the broader economy. It is long-duration and deflationary by nature. And historically, it is a source of outliers, even in turbulent times.

But in this new environment, delivering alpha will require a reset, building portfolios that are even more uncorrelated – anchored by companies with structural product advantages.

Early-stage investors today should focus on a few key principles:

A | Centralized distribution → open-source diffusion

In the last cycle, the dominant path to value creation was achieving scale quickly — one product, everywhere. Today, as globalization fractures, technology must be as flexible, permissionless, and adaptable to local needs as possible.

Open-source and public architecture is best positioned to power this shift.

In a world of ever-changing trade restrictions and rising geopolitical conflict, users and businesses will favor software that is easiest to deploy, modify, and control. Open-source offers the most convenient and frictionless path – minimizing adoption barriers, maximizing local flexibility, and allowing users to extend functionality without waiting on vendors.

There’s historical precedent for this. In the 1990s, open-source encryption moved across borders freely, despite government resistance. Developer collaboration and free distribution outpaced export controls and outperformed centralized, government-sponsored encryption standards.

The same forces are at play today, amplified by AI-driven development, which makes it easier than ever to customize and monetize open-source applications.

Code doesn’t stop at customs. And in a more fractured world, open-source will be the default engine for technology diffusion.

B | Portfolio diversification → portfolio concentration

In the last macro cycle, broad, early-stage indexing could work. You could hold a wide portfolio, and a handful of moderate winners would be enough to drive acceptable returns. Capital consensus could support mediocre products – companies could survive longer by raising the next round, keeping valuations and portfolio marks afloat.

In the new macro, these dynamics are unlikely to hold.

Expect failure rates to rise as underperforming companies lose access to capital. And if foreign investors walk away from U.S. assets, yields continue to rise, and public debt crowds out private investment, allocators will demand even higher returns in venture capital to justify illiquidity and risk.

Without high, concentrated ownership at exit, moderate exits won't move the needle on fund-level outcomes.

Portfolios must concentrate capital earlier and position themselves to be even more uncorrelated — or risk getting sucked into unacceptable mediocrity.

C | Vertical integration → composable architecture

The last generation of software companies won by building proprietary, vertically integrated products. Salesforce, for example, became a $250B company by centralizing customer data, controlling integrations, and expanding its own feature set across a single, standardized platform. This was the fastest path to dominance — both technically (ensuring reliability and control) and commercially (scaling a single platform across rapidly integrating markets).

Today, that model no longer fits.

Customers need software that: (i) flexes to local requirements, (ii) integrates seamlessly into preexisting networks, (iii) enables user-led customization, and (iv) automates workflows across disparate systems. Advances in encryption and AI now make this possible.

On this dimension, the incumbents are trapped. Their economics depend on locking in users and data. They can bolt on integrations and AI automations, but they can't truly open their architecture without cannibalizing the lock-in and rigid product formats that sustain their business models.

In this new cycle, value will accrue to startups built on open, composable systems — architectures that allow users to adapt and orchestrate their own workflows.

This changes how early-stage investors must underwrite companies. It’s no longer enough to evaluate static feature differentiation, data moats, and product roadmaps. They must evaluate the underlying architecture:

Can the system adapt and operate across fragmented environments?

Does the product gain strength as users customize and extend it?

Is there value at the orchestration and coordination layer?

Does the architecture naturally align incentives between users and the broader network over time?

The next $250B software company won't scale by perfecting control and ownership. It will scale through flexible architecture.

The terrain is shifting, but the fundamentals of good investing remain intact. In times like these, clear thinking, and a willingness to interrogate old assumptions and adapt, are the ultimate edge.

Endnotes:

[1] This dynamic is especially pronounced in large-cap tech. Today, the top 10% of S&P 500 companies — led by Apple, Microsoft, NVIDIA, Amazon, Meta, and Alphabet – account for more than half of the total U.S. equity market value. That’s an historic high.

[2] Today, U.S. companies capture ~40% (and growing) of global corporate profits, despite making up less than 20% of global GDP. And ~40% of Magnificent 7 revenue in 2024 came from overseas.

[3] Since 2008, the federal deficit has steadily widened due to slow revenue growth (modest GDP expansion, major tax cuts) alongside rising expenditures (aging-related entitlements, crisis-driven spending, and growing interest payments).